Why personal protection insurance matters more during times of economic uncertainty

As we all teeter with anticipation (and some discomfort) on the cusp of another budget announcement, the sense of economic uncertainty weighs heavy. We can suddenly start worrying about our own financial precariousness, so this month’s article looks at how personal protection might help ease that burden.

In previous articles, we’ve talked about the impact of economic uncertainty on our house buying plans, and how it affects our ability to save for a deposit. And while it’s important to consider how the economy might affect future assets like house purchases, it’s just as valuable to consider how it could impact what we have now.

What is personal protection insurance?

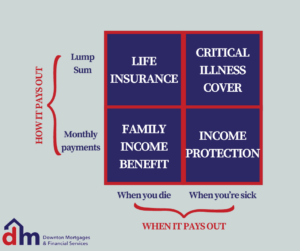

Personal protection insurance is the name given to the suite of insurance products that protect your income and financial security in the case of death, illness or injury. You can read more about them in our personal protection article here, but here is a summary of the 4 main types:

- Life Insurance – pays out a lump sum in the event of your death

- Critical Illness Cover -pays out a lump sum if you are seriously ill (the main reasons people claim are for cancer, heart disease and stroke)

- Family Income Benefit – pays monthly instalments to your dependents in the event of your death

- Income Protection – pays you a monthly income if you’re unable to work due to illness or injury

The impact of economic uncertainty

Economic uncertainty makes the ground beneath our feet shift a little more than usual. Where once we might have relied on a savings buffer or our secure job to get through tough financial situations, we’re now faced with less certainty. When budgets are stretched and savings are smaller, the financial impact of death, illness or injury could be more catastrophic for you and your family.

Financial stress can also put considerable strain on mental health3, increasing some of the risks that protection covers. Having the right cover in place can give you the breathing space you need to get better without further financial burden.

And all of these considerations are particularly important if you are self-employed and don’t have the benefit of employer sick pay. But even if you are employed, it’s worth checking what you’d actually get from your employer, as it’s not always enough.

Reasons you might be avoiding personal protection insurance

When times are hard it’s easy to think that personal insurance is a luxury rather than a necessity. And while cutting costs might feel like the sensible thing to do in the short term, it can make it very hard to weather a financial storm should the worst happen and your mortgage and income are unprotected.

“But the worst isn’t going to happen to me! Right?!”

As a protection adviser, it’s hard not to seem like a doom-monger, but the truth is 1 in 2 people are likely to suffer from a serious illness at some point in their lives1 and 15% of households are taking time off work due to mental ill health2. So it pays to plan for the worst, even if it’s (hopefully) a long way off. What’s more, getting cover when you’re young and healthy can often be more cost effective.

Personal protection is often an undervalued investment, especially when life feels so unaffordable. But irrespective of the economic situation, it’s important to ask yourself if you can afford the consequences of being without it. If you can’t, then it’s worth a conversation with your insurance adviser.

How to get the right personal protection insurance

Personal protection is, by its very definition, unique to your circumstances, and for that reason, it’s impossible to give blanket guidance in an article. The best way to get the right cover is to chat to an insurance adviser and let them find you the most suitable cover. This way, you can be reassured it fits your budget, while also protecting the right things in the right way. Some of the things you might be asked during that conversation are:

- What are your financial responsibilities? g., Mortgage, schooling, child maintenance, etc

- Who is reliant upon your income? g., just you, family, young children, etc

- What level of protection do you currently get from your employer?g., sick pay, death in service, etc

- What is the level of risk you face? – e.g., your health, age, occupation, etc

So, while none of us want to think about worst-case scenarios, it’s helpful to spend a bit of time considering the consequences and planning accordingly if it’s the right thing for you and your family. It’s even harder to prioritise “what ifs” when budgets are stretched and our minds are on other things, but chatting to an insurance adviser and removing some of the worry could be a positive step.

How can Downton Mortgages & Financial Services help?

I set up Downton Mortgages & Financial Services to give people confidence in their financial decisions. We do that by making your options clear and easy to understand. There are no silly questions, and we are on hand to help every step of the way from research through to application.

For more information about our services look at our website here or alternatively, get in touch for a no-obligation chat about your circumstances and house-buying plans.

Sources

1 Cancer Research UK, Cancer Risk statistics

2 Royal College or Psychiatrists – 15% of households taking time off work.

3 Money and Mental Health Facts

Other blogs we’ve written on related topics

Do I need life insurance when I’m young and health?

How would you be able to pay your bills if you were unable to work?

Important Information

The information contained within was correct at the time of publication, but is subject to change (November 2025).

Please note that for all mortgage products, terms and conditions apply. This information is a summary only. You will receive full documentation upon application, which sets out the terms, conditions, and limitations of lending provided.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.